Investment

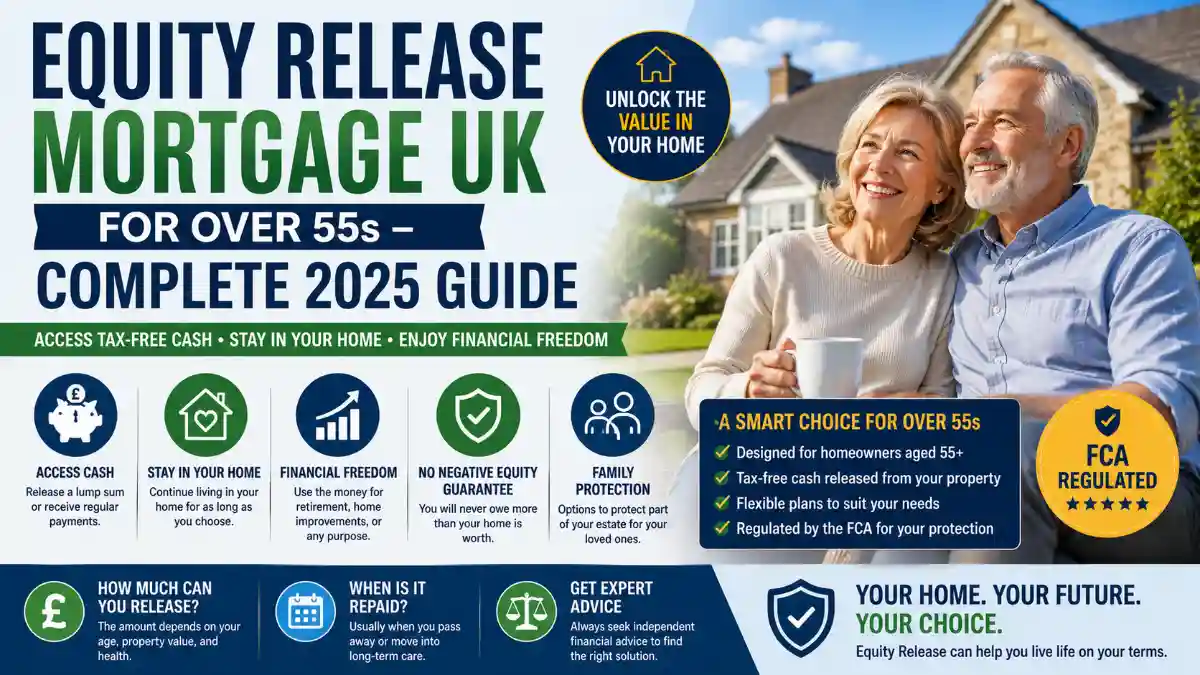

Equity Release Mortgage UK for Over 55s – Complete 2025 Guide

Retirement planning has become increasingly important in the UK as living costs, healthcare expenses, and inflation continue to rise. Many homeowners over the age of 55 are now looking for ways to access additional money without selling their homes or moving to smaller properties. One of the most popular financial solutions in 2025 is an equity release mortgage.

Equity release allows homeowners to unlock tax-free cash from the value of their property while continuing to live in their home. For many retirees, this option provides financial flexibility, helps cover daily expenses, supports family members, funds home improvements, or improves retirement lifestyles.

However, equity release is a major financial decision and should be understood carefully before proceeding. There are different types of equity release products, legal requirements, interest considerations, and long-term financial impacts that homeowners must know.

This complete 2025 guide explains how equity release mortgages work in the UK, their advantages and disadvantages, eligibility requirements, costs, risks, and important advice for homeowners over 55.

What Is Equity Release?

Equity release is a financial product that allows homeowners aged 55 or older to access money tied up in their property without needing to sell the home immediately.

Instead of moving out, homeowners continue living in the property while receiving a lump sum, regular income, or both.

The money released from the property is usually tax-free and can be used for various purposes such as:

- Retirement income

- Paying off debts

- Home improvements

- Helping children financially

- Travel and lifestyle expenses

- Medical or care costs

The loan is generally repaid when the homeowner dies or permanently moves into long-term care.

Why Equity Release Is Becoming Popular in 2025

Several factors are increasing interest in equity release across the UK:

- Rising property values

- Increasing retirement costs

- Longer life expectancy

- Inflation and energy costs

- Limited pension income

- Desire to remain in family homes

Many retirees are asset-rich but cash-poor, meaning they own valuable homes but lack sufficient retirement income.

Equity release helps convert property wealth into accessible cash.

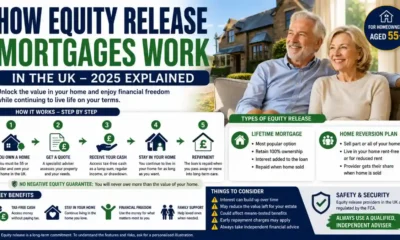

Types of Equity Release in the UK

There are two main types of equity release products available in the UK.

1. Lifetime Mortgage

A lifetime mortgage is the most common type of equity release.

In this arrangement:

- You borrow money against your home

- You remain the owner of the property

- Interest is added to the loan over time

- Repayment usually occurs after death or moving into care

Key Features

- Fixed or variable interest rates

- No monthly repayments required in many plans

- Optional repayment features available

- Tax-free cash access

The loan amount depends on:

- Property value

- Your age

- Health condition

- Lender policies

Older applicants may qualify for larger amounts.

2. Home Reversion Plan

Under a home reversion plan:

- You sell part or all of your property to a provider

- You continue living in the home rent-free or for reduced rent

- The provider receives their share after the property is sold later

This option is less common than lifetime mortgages in 2025.

Who Is Eligible for Equity Release?

Basic eligibility requirements usually include:

- Age 55 or older

- Property located in the UK

- Sufficient home value

- Main residential property

- Property meeting lender standards

Different lenders may have additional requirements related to property type and condition.

How Much Money Can You Release?

The amount depends on several factors:

- Your age

- Property value

- Health condition

- Type of plan chosen

- Interest rates

Generally:

- Older homeowners can release more equity

- Higher property values increase borrowing potential

Some lenders also offer enhanced plans for individuals with certain medical conditions.

Advantages of Equity Release

1. Tax-Free Cash

One of the biggest benefits is access to tax-free money from your property.

This can improve retirement finances significantly.

2. Continue Living in Your Home

Homeowners can stay in their property without needing to move.

This is especially important for people emotionally attached to their family home.

3. Flexible Financial Support

The released money can be used for:

- Debt repayment

- Home renovations

- Family support

- Lifestyle improvements

- Medical expenses

4. No Mandatory Monthly Payments

Many lifetime mortgages do not require monthly repayments.

This reduces financial pressure during retirement.

5. Inheritance Protection Options

Some plans allow homeowners to protect part of their property value for family inheritance purposes.

Risks and Disadvantages of Equity Release

Although equity release can provide financial freedom, it also carries important risks.

1. Reduced Inheritance

Because the loan plus interest is repaid from the property sale later, beneficiaries may inherit less money.

2. Compound Interest Growth

Interest can build up significantly over time if repayments are not made.

This can increase the total debt rapidly over many years.

3. Impact on Benefits

Receiving large amounts of cash may affect eligibility for certain government benefits.

4. Early Repayment Charges

Some plans include penalties for early repayment.

Understanding contract terms carefully is essential.

5. Property Value Risk

Future housing market changes may affect long-term financial outcomes.

Important Features to Look for in 2025

Modern equity release products offer more flexibility than older plans.

Important features include:

- Fixed interest rates

- Voluntary repayments

- Inheritance protection

- Downsizing protection

- Drawdown facilities

- No negative equity guarantee

The no negative equity guarantee ensures you never owe more than your property value.

Drawdown Lifetime Mortgages

Drawdown plans are becoming increasingly popular in 2025.

Instead of taking all money at once:

- You withdraw smaller amounts over time

- Interest applies only to withdrawn money

Benefits include:

- Reduced interest costs

- Better financial control

- Flexible retirement income

Equity Release and Retirement Planning

Equity release should be considered part of a broader retirement strategy.

Homeowners should evaluate:

- Pension income

- Savings

- Investments

- Future healthcare needs

- Family inheritance goals

Professional financial advice is strongly recommended before making decisions.

Equity Release Costs and Fees

Potential costs include:

- Arrangement fees

- Legal fees

- Valuation fees

- Adviser fees

- Interest charges

Comparing lenders carefully is important to reduce long-term costs.

Importance of FCA Regulation

In the UK, equity release providers and advisers are regulated by the Financial Conduct Authority (FCA).

Always choose:

- FCA-authorized lenders

- Qualified financial advisers

- Reputable legal professionals

Regulation improves consumer protection and transparency.

Why Financial Advice Is Essential

Equity release is a long-term financial commitment.

Professional advisers help evaluate:

- Risks

- Suitability

- Tax implications

- Family impact

- Alternative options

Independent advice helps homeowners avoid costly mistakes.

Alternatives to Equity Release

Before choosing equity release, homeowners should also consider alternatives such as:

- Downsizing

- Pension withdrawals

- Savings usage

- Remortgaging

- Family assistance

- Part-time retirement work

Different solutions may suit different financial situations.

Common Mistakes to Avoid

Taking More Money Than Necessary

Borrowing excessive amounts increases long-term interest costs.

Ignoring Inheritance Impact

Homeowners should discuss plans openly with family members.

Choosing Products Without Advice

Professional guidance is extremely important.

Not Comparing Providers

Interest rates and features vary significantly between lenders.

Future of Equity Release in the UK

The equity release market continues growing rapidly.

Key future trends include:

- More flexible products

- Lower interest competition

- Digital application systems

- Improved retirement planning tools

- Better consumer protections

As property wealth continues rising, equity release may become an even more important retirement solution in the future.

Conclusion

Equity release mortgages in the UK can provide valuable financial support for homeowners over 55 who want to access property wealth while remaining in their homes. In 2025, modern equity release products offer greater flexibility, stronger protections, and more retirement planning options than ever before.

However, equity release is a major financial decision that affects long-term wealth, inheritance, and retirement security. Understanding the costs, risks, and repayment structure is extremely important before proceeding.

For many retirees, equity release can improve financial freedom, reduce stress, and create a more comfortable retirement lifestyle. But careful planning, professional advice, and comparing providers properly are essential to making the right decision.

-

Uncategorized1 week ago

Uncategorized1 week agoCivil Construction Foreperson Vacancy 2026 at Fulton Hogan

-

Uncategorized1 week ago

Uncategorized1 week agoGeneral Construction Labourer Vacancy 2026 at Arda Construction

-

Traffic Rules1 day ago

Traffic Rules1 day agoNew Traffic Rules in 2026 Every Driver Must Know

-

Uncategorized1 week ago

Uncategorized1 week agoDelivery Driver Needed at Bidfood Queenstown

-

Job1 day ago

Job1 day agoBest Career Options in Construction Industry 2026

-

Home1 day ago

Home1 day agoComplete Home Construction Process Explained Step by Step

-

Insurance Claim1 day ago

Insurance Claim1 day agoBest Way to Get Maximum Car Damage Insurance Claim

-

Construction1 day ago

Construction1 day agoTop High-Paying Construction Jobs in 2026 That Can Change Your Life